Serious buyers do not need to rush you or confuse you. This toolkit shows how HVAC owners spot lowball offers early, slow the process down, and pull the negotiation back onto their terms.

Key Takeaway: Smart exits are not just about squeezing the highest number. They are about staying in control. When the process feels rushed or unclear, that is usually by design. This Toolkit shows you how to recognize lowball tactics, re-center around your true value, and negotiate with a calm, clear plan instead of fear.

The offer does not show up in a boardroom. It shows up in your inbox between a change order and a warranty issue. You are sitting in the truck after a walkthrough. Crews are packing up. Your phone buzzes. Subject line:

“Excited about next steps”

You open it. The buyer “loves what you have built.” They “see a lot of fit with their platform.” They would like to “move quickly so everyone can get back to business.”

There is a number in the email. It is "higher" than anything you have written down on paper. It is not clear how they got there. The structure is fuzzy. The timing is tight.

They want an answer in a week. They do not call it a deadline, but you feel it. Part of you is flattered. Part of you is tired and tempted. Another part is uneasy.

You start wondering:

• Am I being rushed and lowballed?

• Or is this just how deals work and I should not “overthink it”?

This toolkit is here to answer that before you sign something you regret. Not with hype, not with scare tactics, but with a clear look at the tactics buyers use, the leverage you actually have, and the steps you can take right now to negotiate from strength instead of fear.

Rushed timelines are almost never for your benefit. They exist to get you saying “yes” before you have done the math, organized your numbers, or talked to your advisors.

Reality

• Real deals hold up under scrutiny. They do not need a 48-hour decision.

• Manufactured urgency anchors you on their calendar so you never build your own.

• The more tired and overwhelmed you are, the better this tactic works.

A quiet truth: the wrong offer at the wrong time often looks better than it is simply because it promises relief.

Fix It

• Name the tactic, calmly. “This is a big decision. We are going to move on our own timeline, not yours.”

• Ask for a written Letter of Intent (LOI). No serious buyer should object to putting terms on paper.

• Set your own milestones. Instead of “answer by Friday,” say: “We will respond by [date] after we review this with our CPA and counsel.”

If your business is not truly exit-ready, no timeline will feel comfortable. That is a signal to step back and run a real gut check using “Am I Actually Ready to Sell My Company?”

Pro Move

Flip the urgency. Let the buyer know you are in the middle of a structured review process, not just reacting to the first offer:

“We are currently working through an exit planning process with outside advisors. We will review your LOI as part of that process and get back to you with questions.”

That one sentence tells them:

• You are not desperate.

• You are not uninformed.

• There will be a counter or questions, not blind acceptance.

Quick Win

Before you reply to any “we need an answer soon” message:

1. Close the email.

2. Write down three dates:

• When you will have your numbers cleaned up.

• When you will review with your CPA and attorney.

• When you will respond.

3. Use those dates to set the pace, not the buyer’s suggestion.

You still control the clock unless you hand it away.

Lowball offers rarely announce themselves as lowball. They show up as big headline numbers that quietly shrink once you understand structure.

Reality

• A high top-line price with a weak structure can be worth less than a smaller, cleaner deal.

• Earnouts, seller notes, and “advisory” roles can push real cash far into the future.

• If you do not know your baseline value, every number feels generous or insulting based on emotion.

Fix It

Break the offer apart. Ask for a clear breakdown of:

• Cash at close

• Deferred payments

• Earnout terms

• Any rollover equity or seller financing

Then compare that offer to your true number. That means understanding your adjusted EBITDA and a realistic multiple range for shops like yours, not what you heard someone “got” at the supply house.

If you cannot answer “What is my company likely worth and why?” you are negotiating in the dark. Ground yourself with “What’s My HVAC Company Actually Worth?”

Pair that with our HVAC EBITDA multiple ranges by buyer profile so you have both the framework and the current market data. Walking into negotiation knowing what range buyers anchor on is the most efficient way to spot when an offer is below market.

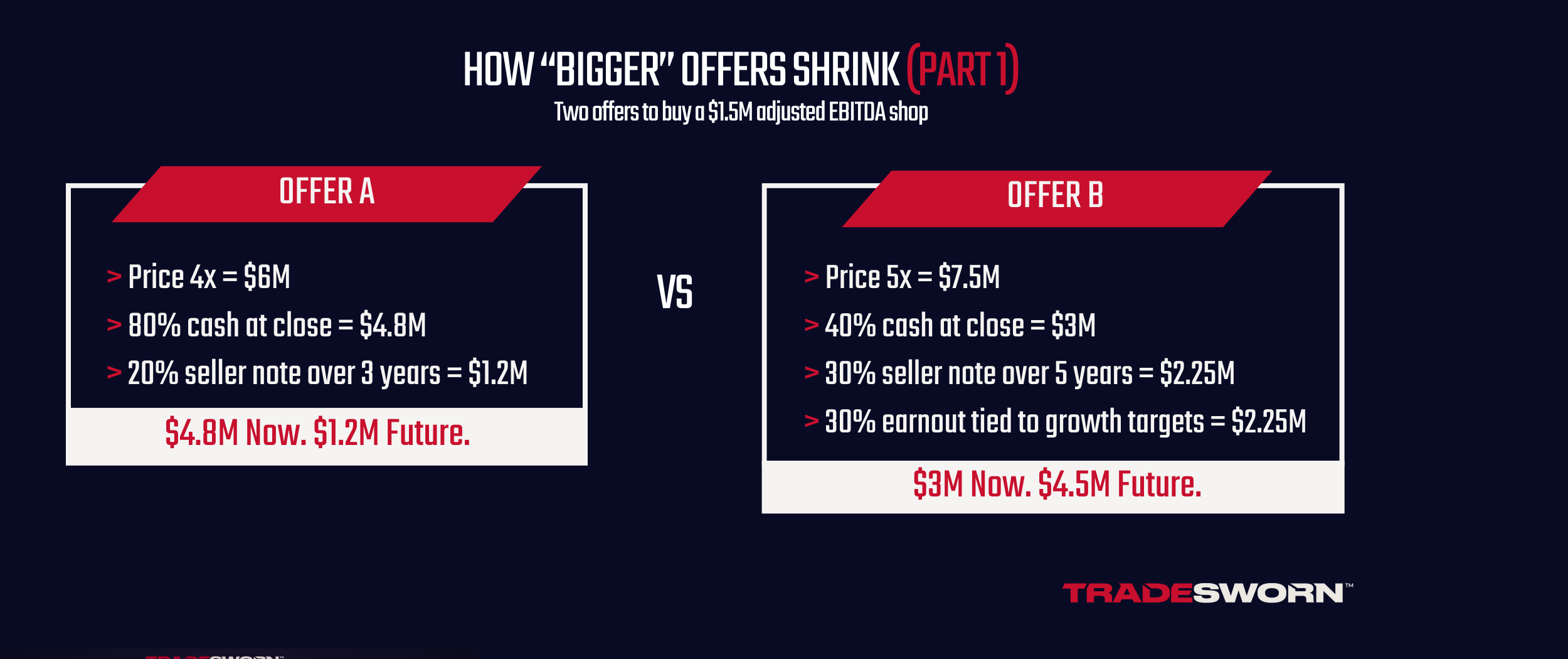

A simple offer example.

Imagine two offers on a shop with $1.5M adjusted EBITDA:

On paper, Offer B looks significantly bigger.

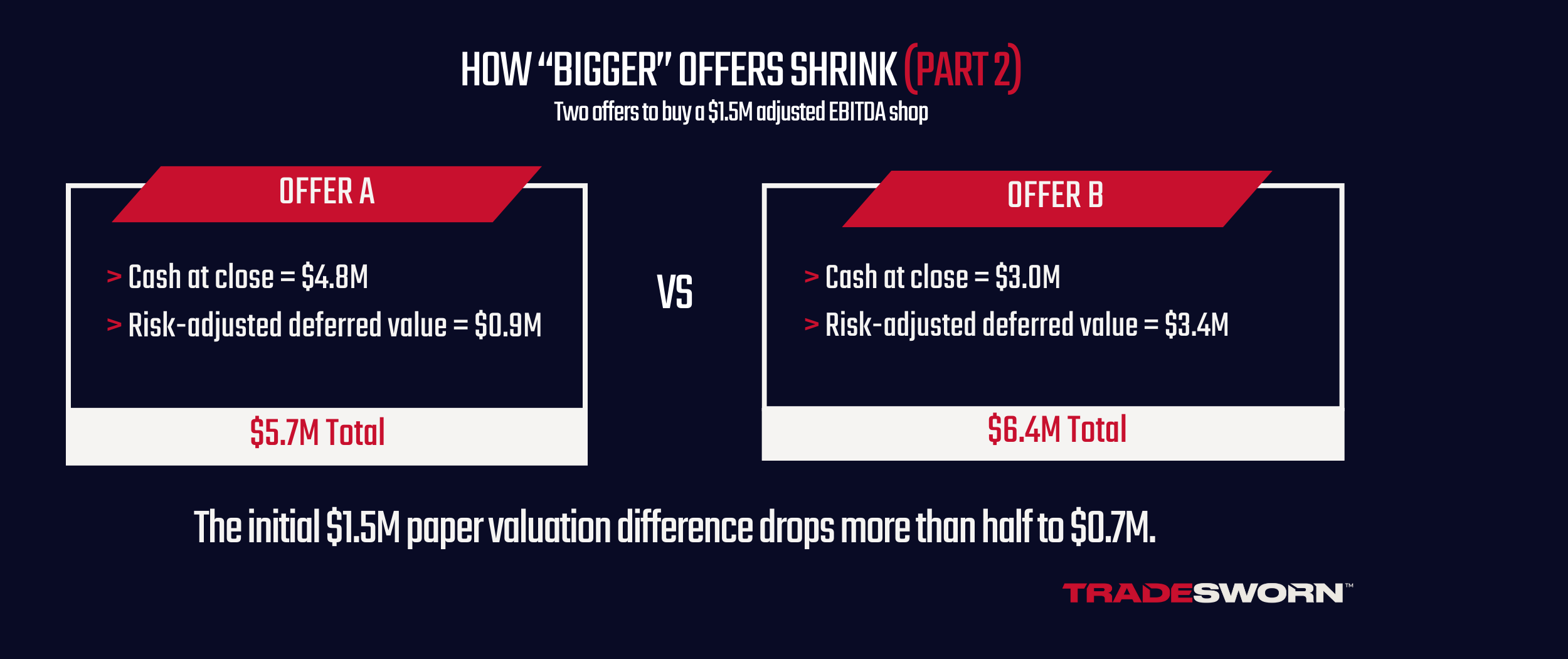

This is a quick stress test, not a full model. In a real deal, buyers also discount deferred dollars for time, buyer credit, and deal terms. For a simple comparison, apply a risk-adjusted haircut (75% realization) to the deferred dollars (seller note + earnout):

• Offer A deferred: $1.2M × 75% = $0.9M

• Offer B deferred: ($2.25M note + $2.25M earnout) = $4.5M × 75% = $3.4M (rounded)

Now compare (cash vs deferred):

For that extra ~$700K after the haircut, you’re taking on much more time and performance risk, plus the stress that comes with it.

Pro Move

Run a quick “would I still be happy?” test on any offer:

1. Reduce all future or performance-based pieces (earnouts, longer seller notes) by 25–50 percent.

2. Ask yourself if the deal still works for your family at that level.

3. If the answer is no, it is not automatically a bad deal, but it's not the slam dunk the headline number suggests.

You are not being pessimistic. You are stress-testing the offer the same way a buyer stress-tests your business.

Quick Win

Once you have a written LOI:

• Schedule a short review block with your CPA or advisor before you respond.

• Ask them to do two things only:

1. Translate structure into “cash I can mostly count on” vs “cash I hope for.”

2. Flag anything that looks unusual for deals in your size range.

Even if they only spot one or two major issues, those points alone can save you more than any “negotiation trick” you would find online.

Confusion is the cheapest way for a buyer to lower your price without ever saying the word “lowball.”

If you are not clear on your numbers, your backlog, or how HVAC deals usually get done, they do not have to be aggressive. They can simply act doubtful.

Reality

• Vague phrases like “industry norms” and “market risk” can hide a thin justification for a low multiple.

• Buyers will probe your understanding of margin, customer concentration, and recurring revenue.

• The less confident and specific you are, the more they feel justified in discounting.

Here is the contrarian piece: trying to rush through the entire process “just to get it off your plate” often signals to buyers that you are more tired than prepared. Tired sellers rarely get top-of-market terms.

Fix It

Clean up your house and protect your sell price:

If you feel like your confusion is coming from burnout, not just from the offer, use “How Do I Exit Without Burning Out?” to stabilize yourself before you negotiate.

Pro Move

Treat confusion as a signal to slow down, not speed up.

When something does not add up, say:

“I appreciate the offer. Before we move forward, we need to reconcile these numbers against our internal reporting and how HVAC deals are typically structured. Let’s walk through your assumptions in more detail.”

You are not accusing them of anything. You are showing that you are the kind of seller who checks the math.

Quick Win

Run the Buyout Potential Scorecard on the Scorecards page:

• It forces you to look at recurring revenue, margin resilience, service mix, and customer concentration the way a buyer does.

• It gives you a score you can anchor around instead of reacting to whatever anchor the buyer throws out.

Once you see how your shop scores, lowball offers are easier to spot and easier to walk away from.

The hardest time to negotiate is when you are exhausted and surprised. That is exactly when many HVAC owners get their first serious offer. You cannot control when buyers show up. You can control how prepared you are when they do.

If you want to see the scale at which buyers are actively building HVAC platforms right now, read S&P Global Market Intelligence reporting on private equity’s appetite for HVAC add-ons so you stay calm, slow the process down, and do not treat the first LOI like your only option.

Reality

• If you treat the first LOI as your only shot, you give away leverage you did not realize you had.

• Most of the value in an exit is built months or years before any offer appears.

• The owner with a plan will almost always beat the owner who is just reacting.

Fix It

Shift from “Do I take this?” to “How does this fit my Exit Workplan?”

A real Exit Workplan gives you:

• A clear Buyout Potential Score so you know where buyers will push.

• A grounded valuation based on how HVAC deals actually price, not just rumor.

• A targeted buyer map so you know who else might be interested and why.

• A strategy call so you can line up your personal goals with the math, not trade one against the other.

That way, when an offer comes in too fast or too low, you have options:

• Say no and keep building.

• Counter with confidence.

• Talk to other potential buyers from a position of strength.

Pro Move

Before you answer any buyer, write down three statements:

1. “Here is what my business is roughly worth based on current numbers.”

2. “Here is what I actually want out of a deal.”

3. “Here is the timeline I am comfortable with, whether this buyer stays or walks.”

Keep that paper next to you when you negotiate. You are less likely to drift into decisions that match their priorities instead of yours.

Quick Win

Take the Score Your Shop diagnostic first. It takes less than a minute and checks the five signals buyers quietly watch for early:

• Jobs per month

• Team size

• Schedule load

• Cash position

• Operator confidence

This gives you a clean baseline so you can judge the offer against your real operating strength, not their deadline or their headline number.

You do not have to take the first offer. You do not have to race their clock.

You get to decide whether an offer is a real opportunity or just pressure in a nice suit.

When you understand how the clock, the structure, and the confusion game work, you are much harder to rush and much harder to lowball.

If pressure or confusion is driving the conversation, slow it down. “Fast” is a negotiation move more often than it is a favor.

If your situation looks like this, the headline number looks decent but the terms feel off, start with What’s My HVAC Company Actually Worth?. You need a baseline before you debate structure.

If the offer showed up before you felt ready, use Am I Actually Ready to Sell My Company? to see which gaps might be feeding their leverage.

Then choose the right support read:

• How Do I Exit Without Burning Out? if exhaustion is driving the “maybe I should sell” impulse.

• What’s Really Stalling My Exit: Me Or The Business? if the real issue is timing and clarity, not the deal in front of you.

Run the Buyout Potential Scorecard before you negotiate so you can spot the risks a buyer is pricing. When you want leverage you can actually hold, request your Exit Workplan.

Here are the top toolkits HVAC owners are reading, using, and sharing to work smarter every week.

Burnout shows you exactly where the business leans on you too hard. Setup weekly owner blocks, hand off 1 choke point, and survive the exit process.

Two shops with the same profit can be worth $1M+ apart. Learn how buyers price risk and EBITDA, then improve your number before you sell.

If an exit feels stuck, it is usually uneven readiness. Spot the real blocker and build a shop that clears diligence cleanly, without panic fixes.

Smart exits don’t start with a broker, they start with a scorecard. Use this checklist to see if your business is truly ready, or just busy.

No spam. Get real advice and proven tactics to win more jobs and keep more profit.

“We cut the noise, ran the plan, and made more in two quarters than we did all last year.”

— Sean, Massachusetts